The Atlantic hurricane season officially started on June 1, and anyone living in areas prone to hurricanes who hasn’t already prepared for it should get ready now. According to an article in SHRM: Society For Human Resource Management, the National Oce…

In recent years, employers have paid millions of dollars in back pay to workers who have been classified incorrectly or paid for fewer hours than they should have been. Both federal and state laws apply to employers, and some of the requirements are co…

For employers and their employees, past and present, there may be a few issues that you need to consider before enrolling through products sold in the Federally-Facilitated Small Business Health Options Program (FF-SHOP).

Nestled among the multiple emails received last week from the regulatory agencies over the Patient Protection and Affordable Care Act (PPACA), under the heading of FAQ Updates on the SHOP, Agent-Broker – Other is FAQ 1955. The short FAQ announces that the Consolidated Omnibus Budget Reconciliation Act (COBRA) transactions will not be supported in the FF-SHOP Exchange for small businesses as of November 15, 2014, but will only be supported in a future release. The FAQ can be found here: https://www.regtap.info/faq_viewe.php?i=1995

For small employers that meet the requirements to offer COBRA continuation to their former employees or dependents, the FF-SHOP will not be an option, even if they qualify for the Small Business Tax Credit (SBTC). While the Department of Health and Human Services (HHS) and Centers for Medicare & Medicaid Services (CMS) work out the information technology on how to allow for these transactions, any tax credit the business would qualify for would be quickly negated with the $100 per day fine for each qualified beneficiary entitled to COBRA. So, if a family of four qualified for COBRA, that would be a $400 per day fine for each day they were not given notice, or for each day they were not allowed to enroll in that coverage. COBRA, which is enforced by the Department of Labor (DOL), has been around for several decades for employer groups that have more than 20 full-time equivalent employees working at least 50% of the days of the prior calendar year. Controlled organization rules also apply in determining the count. It is not likely the DOL will allow for any transitional relief for this issue given how long the laws have been in place.

This also brings into question whether this FAQ would also be applicable to states where “mini-COBRA” must be offered. These “mini-COBRA” rules apply to employers in states that have enacted continuation laws for groups that do not meet the federal requirements. These groups have fewer than 20 full-time equivalent employees. Not all states have these requirements, but many do and this will likely also be problematic for them to utilize the FF-SHOP initially. This will likely be a concern, even though no official word has been released yet from HHS or CMS, on this issue.

For employee consideration, a new COBRA model election notice was released several weeks ago to include a statement about options in the individual Marketplace. However, the federal or state continuation may be the persons’ best option versus going to the Marketplace for coverage. In many areas of the country, the individual Marketplace products have higher deductibles and out of pocket maximums than the group coverage. There is likely no deductible credit on the individual product, so if they have already met it this year on their group plan, they will start all over again. Also, there may be limited networks offered in the individual Marketplace products, or even a limited choice of insurance carriers.

It will likely be in the employers’ best interest to delay utilizing the FF-SHOP, at least until the issues have been worked out surrounding COBRA continuants.

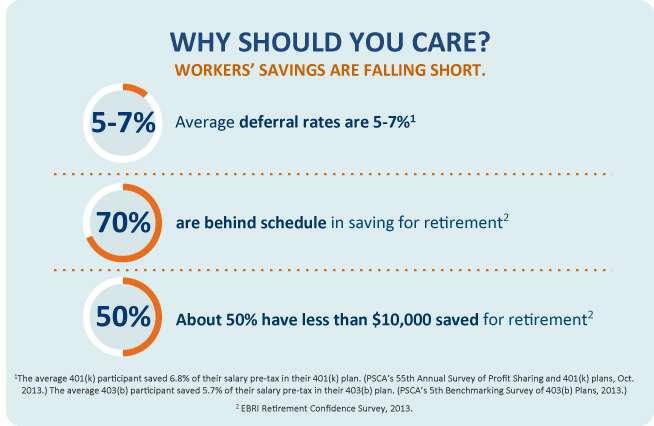

There’s no denying it. The vast majority of workers won’t be ready financially for retirement. Seventy percent are behind schedule in saving for retirement and half of all Americans have less than $10,000 in savings. Of immediate importance is the fact that nearly half of the oldest boomers are at risk of not having sufficient retirement resources to pay for basic retirement and healthcare costs!

Why should you care about retirement readiness? The answer is simple: Because retirement delays can hurt your bottom line.

The majority of employers expect the cost of healthcare and other benefits to rise due to delayed retirements. And they’re exactly right. In fact, for each employee over the age of 65, a plan sponsor could be paying $5,000 more per year for health care. (Source: EBRI Estimates)

In addition, the cost of employees working beyond the normal retirement age can have potentially significant implications for your business as a whole.

So how do you know if employees are saving enough, and how do you measure success?

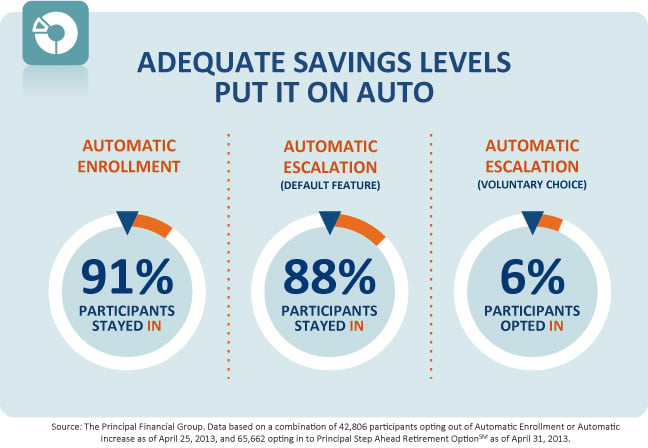

Simple plan design changes can have huge impacts on participant outcomes. Features like automatic enrollment and automatic deferral increases, for instance, use participants’ inertia to their advantage.

In fact, 91% of participants stay in the plan when automatically enrolled. And 88% of employees participate in an automatic escalation program when it’s a default feature—only 12% opt out. But when they have to sign up on their own, just 6% participate.

UBA, in partnership with Principal Life, are hosting the complimentary webinar “Breaking Through the Barriers to Create Retirement Plans that Work for Everyone” on Thursday, June 19, 2014 at 2:00 pm EDT / 11:00 am PDT.

Webinar attendees will receive practical tips on how to:

Evaluate a plan to determine the income replacement ratio

Determine if effective plan design features are in place

Implement plan design changes to help employees retire on time

To register for the webinar, visit UBA’s WisdomWorkplace webinar series at http://bit.ly/1hzjaTW and enter code UBAPFG to receive the complimentary $149 discount.

As the cost of employer-sponsored health insurance continues to rapidly outpace wages and inflation, now more than ever employers are looking for ways to keep costs down. One way to do so (that requires very modest investment) is by improving benefits communication, a critical component of employee engagement.

Industry research has shown that employees have a positive perception of their benefits (even when the overall package is mediocre) if there is an excellent communications plan in place. Unfortunately, three out of four employees say they need more education to understand how changes in their benefits affect their financial safety net*.

And, as more and more employers move to high deductible health plans, making employees aware of how to use their benefits and take control of their health care consumption will be the key to cost savings.

UBA’s white paper, “A Business Case For Benefits Communications,” addresses how best to reach employees, what they need to know, and how they prefer to receive the information.

For example, here are a few examples from the white paper:

HIDDEN PAYCHECKS

Total compensation statements, or “hidden paychecks,” serve as excellent ways to inform employees about what the company is providing for them. These statements not only outline an employee’s wages but also display the employer’s contributions to benefit plans such as medical, life, retirement, and more.

MAKING EMPLOYEES ‘STEWARDS’ OF THE PLAN

Sharing the financials associated with the health plan and other benefits help employees understand and become ‘stewards’ of the plans, wanting to become better consumers and help control costs. It’s helping employees understand what they can and can’t control in the health care puzzle.

BENCHMARKING DATA

Communicating benchmark data about how an employer’s plan compares with those of other companies is another way to drive home the value of a benefits package.

“We use the benchmark data from the UBA Health Plan Survey to compare not only benefits, but contribution levels,” says Andrea Kinkade, president/employee benefits advisor with Kaminsky & Associates, a UBA Partner Firm in Ohio. “We even use it during open enrollment meetings to illustrate how our clients’ benefits and contributions levels are better than their peers. It is an extremely beneficial and key part of the renewal process as many companies struggle with what level of coverage to offer and how much cost sharing to include. When their benefits exceed the benchmarks, it is a great reminder to employees of just how good a medical program they have.”

Download a copy of UBA’s white paper today for an in-depth look at employee benefits communication strategies: http://bit.ly/1gJR3GE.

The regulatory agencies have recently issued two sets of guidance that affect an employer’s Consolidated Omnibus Budget Reconciliation Act (COBRA) obligations and opportunities under the Patient Protection and Affordable Care Act (PPACA).

Special Enrollment for COBRA Beneficiaries

Under the Marketplace special enrollment rules, a person who has a COBRA qualifying event may enroll in a Marketplace policy as a special enrollee when the person first becomes eligible for COBRA. A qualified beneficiary also may enroll mid-year as a special enrollee when COBRA expires. In both of these situations, the person is eligible to apply for a premium subsidy. However, a qualified beneficiary may not drop COBRA part way through the coverage period to enroll in Marketplace coverage – unless he or she does so during open enrollment.

The regulatory agencies were concerned that qualified beneficiaries did not understand these rules and therefore the federally-facilitated Marketplaces are offering a special enrollment period until July 1, 2014. According to guidance issued by the Department of Health and Human Services (HHS) on May 2, 2014, during this special enrollment period qualified beneficiaries may drop COBRA and enroll in the federal Marketplace. (State-run Marketplaces may, but are not required to, offer this special enrollment period.) Employers are not required to notify qualified beneficiaries of this special, extended enrollment period, but they may wish to do so.

Updated COBRA Notices

The Department of Labor (DOL) has updated both the model General Notice of COBRA Continuation Rights and the model COBRA Continuation election notice to include information about the Marketplace. The model general notice now includes basic information about Marketplace coverage and includes a Web address the participant can consult for more information. The model election notice, which was revised in 2013 to include information about the Marketplace, has been revised again to include more detailed information about Marketplace coverage, rules, and options. Employers are not required to re-distribute the General Notice, but they may wish to provide it as part of the next open enrollment period to help ensure that individuals who become COBRA-eligible consider the possibility of purchasing Marketplace coverage, rather than COBRA.

The election notice still must be provided to new qualified beneficiaries within 14 days after the plan administrator is notified that a qualifying event has occurred. There is also a 30-day period for an employer to notify the plan administrator that a qualifying event has occurred, so in many cases the notice does not need to be given until 44 days after the qualifying event. Employers may wish to provide election notices well before the deadlines to give qualified beneficiaries adequate time to choose between COBRA and Marketplace coverage, since the special enrollment period for Marketplace coverage ends 60 days after employer-provided coverage ends.

There is no deadline to begin using the updated notices, but employers should begin using them as soon as they can. The notices are models, so the employer may modify them to better fit its situation.

For further information about the health care reform requirements for your business, download UBA’s complimentary guide, “PPACA Compliance and Decision Guide for Small and Large Employers” from the PPACA Resource Center at http://bit.ly/1nHbaWv.